Of What Use is Deferred Tax Expense to Financial Analysts?

Interperiod tax allocation has been required since the 1950s, soon after Congress permitted tax deductions based on accelerated depreciation of long-lived assets. History indicates that the accounting standard setters who pushed for interperiod tax allocation (ARB 44 and APB 11) were fighting the good fight against issuers.

Notwithstanding such good intentions, I took the position in my previous post that on conceptual grounds at least, interperiod tax allocation has been an unnecessary and costly aspect of U.S. GAAP (and IFRS). It is common knowledge that using tax deductions at a faster rate than the economic depreciation of the asset burdens management: it causes opportunities to dispose of the asset less attractive on an after-tax basis.

But, a burden does not always equate to an obligation:

“According to any reasonable understanding of the word, obligations are incurred independently of how financial statements are prepared, and they would be incurred even if financial statements were not prepared.”

[Leonard Lorenson, AICPA Research Monograph No. 4, Accounting for Liabilities, 1992. Italics in original]

Consistent with that observation by Leonard Lorenson, my example in the previous post demonstrated that recognition and measurement of a deferred tax liability solely depends on how other assets and liabilities are recognized and measured. Many different types of events or decisions can impose a burden on a company, but only a subset will qualify for liability recognition.

Moving from Conceptual to Practical: The Matching Argument for Deferred Taxes

To provide you with a fuller explanation of my views on deferred tax accounting, I also need to challenge what I regard as its main practical justification: that interperiod tax allocation supposedly results in more appropriate measures of net income. This is known as the “matching” argument. When APBO 11 was superseded by SFAS 96 (which due to implementation issues was ultimately replaced by SFAS 109) the FASB switched to the asset/liability argument from the “matching” argument.

Matching calls for attributing an appropriate amount of tax expense to a given amount of reported NIBT. For example, if: (1) statutory tax rates are constant over time (say, 40%); and (2) the only differences between a company’s taxable income and its reported NIBT are timing differences, the appropriate amount of tax expense to attribute to the period would be 40% of NIBT. Note that this makes proponents of matching completely indifferent to whatever the tax return for the current period might indicate as currently due to the taxing authorities. More important, though, is that the acid test of the matching argument should be whether reported net income is a good predictor of future net income.

As with the asset/liability argument, let’s begin with a simple example:

Company A purchased a machine for $15,000. For financial reporting purposes, it will depreciate the machine on a straight-line basis over 5 years with no salvage value for financial reporting purposes. It will use the double-declining balance (with a switch to straight-line after 3 years) depreciation for tax purposes. In all five years, net income before taxes and depreciation is expected to be $9,000 and the tax rate is 40%.*

Next, I need to introduce two tax rate concepts. First, SFAS 109 defines the “effective rate,” as:

(Current tax expense + Deferred tax expense)/NIBT

If interperiod tax allocation is useful for financial analysis, the effective rate should generate valid expectations about future cash outflows for income taxes.

An alternative analytical ratio to the effective rate would be the “current rate” calculated as:

(Current tax expense)/NIBT

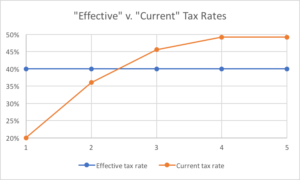

This graph compares the values for these two ratios for the five years covered by the example.

It plainly shows that in the periods immediately after the “taxable difference” originated, the effective tax rate is higher than the current tax rate. But in subsequent periods, the effect on total tax expense of interperiod tax allocation is reversed. That is because the difference is solely due to timing.

But, the key for understanding the practical impact of interperiod tax allocation is the effect in the earliest periods. That’s because this is the effect we should expect to see in the financial statements of, in contrast to my static example, dynamic companies.

Let’s stipulate that the differences between book values and tax bases of non-current assets account for a large and persistent portion of the deferred tax liability for firms with moderate to high capital intensity. Since replacement costs of assets usually exceed historical costs when there is even a moderate amount of inflation, their total timing differences should usually net to taxable differences (as depicted by the first two years in the graph) even though they will decrease for individual assets (like the later years in the graph). Generally, only firms whose productive capacity is shrinking faster than the rate of inflation will have periods in which new taxable differences are less than reversals of old taxable differences.

Twenty years ago, I conducted, but did not attempt to publish, an informal test of the proposition that reported current rates would be persistently lower than effective rates. I analyzed the public companies in the Compustat PCPlus database for the years 1977 to 1996 that met the following criteria:

- Calendar fiscal year-end

- U.S. company in an industry other than financial services

- Current and deferred income taxes are reported for all 20 years.

I calculated the effective and current tax rates by year for each of the 546 companies that met these criteria. This is a graph of the results:

If the effective tax rate were a good long-run measure of taxes paid, we would expect to see that median current tax rates would exceed effective rates roughly 10 times of the 20 years studied. It didn’t happen even once.

A closer look reveals that the difference between effective and current rates widened at first. This is consistent with the view that timing differences were increasing, due to a combination of inflation and real growth. One might attribute the large decrease in the difference occurring in 1988 to the effect on deferred tax expense of various methods first used to transition from APB 11 to SFAS 96, and then to SFAS 109. The effect of transition for many firms was to reduce deferred tax liabilities previously recorded, thereby recognizing significant deferred tax benefits, which artificially and temporarily reduced effective tax rates. Perhaps the difference started widening again around the time that SFAS 109 had been adopted by all U.S. firms.

Thus, the intuition that the practical basis for interperiod tax allocation is highly questionable has some empirical support. Yet, interperiod tax allocation appears to have one practical, albeit cynical, use: to obscure how little income taxes corporations are paying relative to statutory rates.

My understanding is that APBO 11 passed by the narrowest of margins (the Accounting Principles Board needed a 2/3 vote to issue a new Opinion). Preparers resisted it strenuously, and at least two of the Big Eight firms opposed it — either for principled reasons or due to pressure from their clients.

That would certainly challenge the justification for my cynicism, but APBO 11 was issued nearly 50 years ago. Perhaps there has been little resistance since then to deferred tax accounting as corporations have now come to see it as working to their collective advantage—by fixating the public on effective tax rates, which generally hover around the statutory rate. To be sure, the financial press will publish anecdotes of high profile tax avoidance cases, but that’s not the same as financial statements pervasively reporting low rates of tax expense.

Whatever the reason, the fact remains that we are living with a complex system of measuring income taxes. A simpler and more transparent method would suit users of financial statements just fine.

———————

*My full spreadsheet is available here.